PlatON Column | Let’s talk about the stablecoin of Japan as a goodbye to the volatile 2022 By James QU@PlatON from Tokyo Dec.31.2022

Want to talk about stable coin at the end of 2022 after experienced super high volatility in crypto world. Wish stable and healthy next year! Happy new year to everyone!

We are in the mid of dramatic shifting from web2 to web3, where the real world has a well established legal framework for web2, and it is NOT ready for web3. When conduct a real business on web3, the entrepreneurs are having difficult time handling regulation issues, such as cannot finalize business model and settle the deal due to lack of legal support. Current way of organic grow is a a mix of web2 and web3, which means following existing legal requirements by leveraging web2 platforms and tools, and reduce cost (faster and cheap settlement) by introducing web3 way of doing business.

Most of time web2 platforms here means the existing system covers license, kyc, aml, investor protection, regulatory reporting and legal documentation etc, which are mandatory to complete any deal in current real world under existing regulation framework.

Look at Japan, it is building up web3 infrastructure step by step

- legally defines qualified crypto tokens as a financial product, can be traded via regulated (licensed) financial exchange service providers which in turn defines the fair value for each token

- Security Token (STO) based by real asset can be legally traded

- Regional utility tokens, stable coins, asset based tokens are issued

- Open the door to global stable coins next year

- Amended institutional start ups STO (ICO) tax policy to boost crypto innovation

Overall, the law framework is well established, and is adjusting along with crypto technology progress.

Today I will share my personal views after reading papers from Progmat project, which is a good example of mixed web2 and web3.

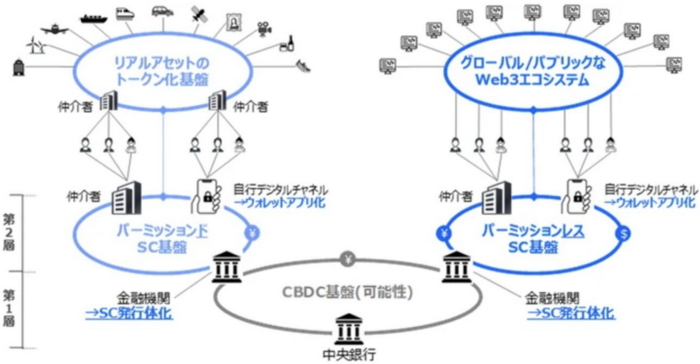

Stablecoin (SC) can be divided into different categories according to the form of the chain (consortium/public chain) and the way of issuance (whether it is licensed, or real assets-based, or algorithm-based). The following are some examples:

1.public chain issued by central bank

2.Consortium chain issued by central bank

3.public chain issued by licensed institutions

4.public chain issued, algorithm based, non licensed

5.consortium chain issued, licensed and real asset backed,

Elements of security tokens (ST)

1. Clearly defined as assets and supported by assets;

2. Presenting the existing assets or privileges;

3. With complete asset governance (private key management);

4. With a feasible and verifiable trading mechanism and settlement mechanism.

Let’s look at Progmat, a stablecoin platform.

A DLT infrastructure for Market Transformation and New Market Creation, deliver digital transformation of the so called value chain of financial transactions and creating new markets.DCC, Digital Asset Co-Creation Consortium, let by MUFG, with more than 134 members ( by end of Sept, 2022 ) aims to innovate new digital asset ecosystem cross industries operating on top of Progmat platform.

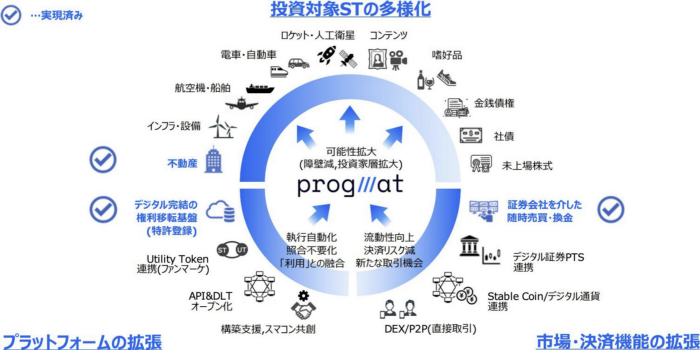

Progmat has achieved the business expansion and innovation in the following aspects:

- Platform expansion: Seamless inter-organizational collaboration will enable automated execution and free of reconciliation, as well as the integration of “investment x utilization” of Security Token (ST) and Utility Token (UT).

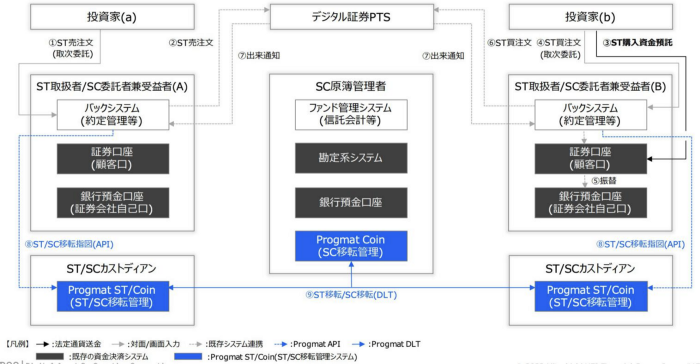

- Expansion of market and settlement functions: Improve liquidity and minimize settlement risk and intermediary costs through digital securities PTS, Stable coin (SC)/Digital Currency, and DEX.

- Diversification of Security Tokens (STs) for investment by leveraging above to creation of unprecedented product markets through elimination of existing practical barriers and expansion of new investor base.

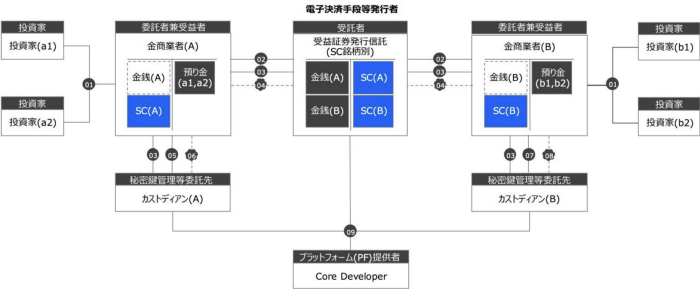

Participants and related financial tools:

- investors, trustees, agents, beneficiaries

- Financial institutions

○ such as PTS exchanges and other financial service providers

○ Custodian

○ Asset management firm

- Progmat platform with program coin, operating consortium

- CBDC issued by central bank

- Stable coin issuers, utility coin issuers as part of financial infrastructure

- ST Issuers, NFT issuers, etc. Institutions provides financial products.

Existing regulation framework

- Financial Instruments and Exchange Act

- Order for Enforcement of the Payment Services Act)

- Act on Sales, etc. of Financial Instruments

- Foreign Exchange and Foreign Trade Act

- Act on Prevention of Transfer of Criminal Proceeds

Note: Names of Laws and Regulations, FSA Japan

The two layers architect

Business flow

- Stable Coin issuers flow

- Typical Security Token transaction flow

There are many other cases, will not share here

Here is how Progmat solves common issues about cross-chain transactions:

- Cross-chain connectivity and authentication: After verified Trusted Third Party (TTP) vs Hashed Time Locked Contract (HTLC) vs Relay, Progmat will use Relay as the primary way

- Cross-chain architect: Leverage TEE proxy based on IBC protocol, implementation was on Corda

- Cross-chain test was done on Quorum-Corda

It is clear from the development of Progmat that only regulated institutions can be SC issuers and service providers. Investor protection and personal information protection remain a top priority. Transaction finalization based on SC, asset reservation is required, a kind of proof of reservation in web2 style.

This article is reproduced from https://platon-network.medium.com/lets-talk-about-stablecoin-of-japan-as-a-good-bye-to-the-volatile-2022-fe5593daf072